Comprehensive guide to private health insurance in Spain for expats: meeting visa/residency requirements, comparing insurers (Adeslas, Sanitas, ASISA, Mapfre, AXA), pricing by age, pre-existing conditions, age limits, and insider tips from our partnerships with major insurers.

Health insurance. I hate it. As a Canadian it just rubs me the wrong way to even consider paying for health services out of pocket and be forced to navigate the murkey actuarial waters of health profiteering. That said, if I have to live in a healthcare system that integrates private health insurance, I'll take Spain's healthcare system any day. It's extremely cost effective (see Spain's healthcare rankings), the insurance market is very competitive, and coverage is ubiquitous.

But buying private health insurance is one of the biggest pitfalls in the visa application process and a challenge for many of us who aren't used to private health insurance systems (mostly those outside of the US). It can be one of the biggest monthly expenses for families, in some cases exceeding the cost of the family car. This guide attempts to break down some of the important terms and educate our audience about an industry that sometimes thrives on our ignorance.

This guide is "semi-insider" because in 2020 Spain Expat started building partnerships with honest, transparent health insurance agents at each of the major private insurers in Spain in order to power the first private health insurance comparison tool for expats seeking health insurance for their visa or residency. In the process of building these relationships and tools and helping hundreds of expats, we learned a lot more than the average health insurance shopper and got a peek behind the scenes. This is the practical information guide we wish we had when we went shopping for our health insurance in Spain.

And yes, as noted, we have relationships with almost all of the insurance companies mentioned in the article – that's the only way we could stay objective!

Expat health insurance is generally referring to the types of policies that are considered "full coverage" for normal Spanish residents, not travellers, and are required for most visa or residency applications. These requirements vary somewhat from consulate to consulate but the Spanish government's overarching law requires all people living in Spain to have some sort of health coverage (public or private insurance), period. Whether the consulates require you to have private health insurance is debateable, though for most of us it's generally true with some exceptions. For the 99% of us without any cause for exception, we will be buying private health insurance policies that meet the typical requirements set by the consulates; in particular policies that do not have co-pays or deductibles.

Travel medical or health insurance, as you'll see in the Consular Requirements section, is rarely permitted for visa or residency applicants coming from the English-speaking world, such as Canadian citizens, US citizens or UK citizens, but much more commonly accepted from non-English speaking countries in Latin America or Asia where, generally speaking, visa requirements are somewhat more lax.

| ASISA Price Per Use * (capped at a maximum of 300€ per year) |

|

|---|---|

| Nursing, and podology | € 1.50 |

| GP and paediatrics consultations | € 5 |

| Emergencies (hospital and home visits) | € 17 |

| MRI/CT scan/PET | € 50 |

| Physiotherapy (per session) | € 3.50 |

| Preparation for childbirth (per session) | € 27 |

| Psychotherapy (per session) | € 13 |

| Other services (per session) | € 8 |

| *source: www.spainexpatinsurance.com/asisa/ | |

"Co-payments" (U.S. parlance) aka "excess payments" (U.K. parlance) are "pay-per-use fees" (insurance company parlance) that you, the policy holder pays at the time of service directly to the provider to offset costs and disuade frivolous expenditures. They usually range from 5€ to 50€. See examples of co-pays/excess payments in the ASISA Price per use table.

Deductibles are an annual cap on total expenditures that you, the policy holder, have to pay ("out of pocket") before the insurance company starts paying for everything else. There can be deductible limits for the individual and/or for the family too. Deductibles exist to offset their payouts against the most common costs a policy holder generates, like doctor's visits when you're ill, while ensuring that in a bad situation you're not going to have runaway costs that bankrupt you. In the ASISA Price Per Use table you'll see the "capped at maximum of 300€ per year" is the deductible limit for their policies that have co-pays and deductibles.

Without deductibles and copays, policy prices are generally about double those of a similar policy, which is what we, as expats, are forced to pay in order to meet the requirements of the consulates for our visa application.

Note: ASISA also offers policies without deductibles and co-pays that qualify for your residency or visa application. You can get a quote and compare their co-pay vs no-co-pay prices very easily here: www.spainexpatinsurance.com/asisa/

Why do the consulates require us to have such expensive policies? Of course we can afford the extra 300€ per year for the deductible if we get to save 400€ or more on the policy, right?

The consulates want to ensure we are 100% covered for everything and bear zero risk of forcing the government to clean up a financial mess in case of an accident or serious illness that leaves you destitute. It's laid out as follows in Order PRE / 1490/2012 (translation linked):

c) People who do not carry out a work activity in Spain must provide documentation proving compliance with the following two conditions:

1. Public or private health insurance, contracted in Spain or in another country, provided that it provides coverage in Spain during your period of residence equivalent to that provided by the National Health System.

It will be understood, in any case, that pensioners meet this condition if they prove, through the corresponding certification, that they have the right to health care at the expense of the State for which they receive their pension.

So, not all expats living in Spain require health insurance. Pensioners can get public healthcare paid for by their home government, as is the case with the S1 application for UK pensioners residing in Spain. But that's a different article. For the rest of us, there's only private health insurance to meet the requirement of equivalent healthcare to that provided by the National Health System of Spain.

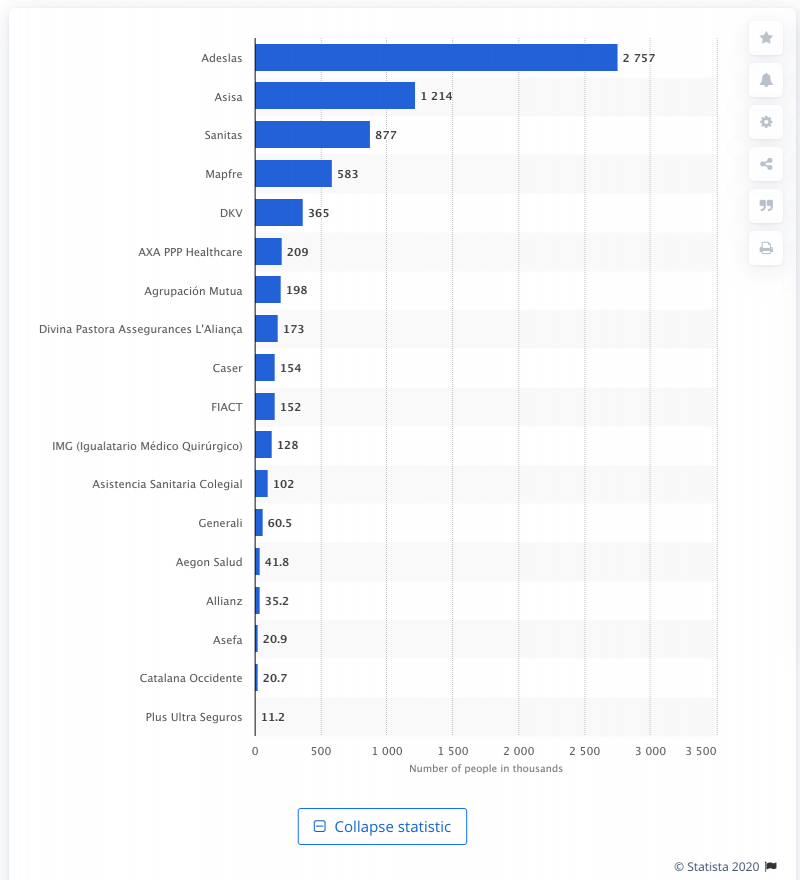

Ranked list of health insurance companies in Spain based on number of customers in 2019

Ranked list of health insurance companies in Spain based on number of customers in 2019In Spain the major health insurance companies that provide nation-wide coverage (with a few exceptions for areas like the Basque Country and Cantabria due to having their own local systems) are the following:

Yes, the Trustpilot reviews are bad, but have you ever looked up your health insurance company from back home? Consider yourself warned. The industry often struggles to meet customer expectations, and for good reason. See my brief rant at the beginning of this article. That said, 95% of the expats that responded to my questions on expat Facebook groups are happy with their health insurance providers in Spain, and the level of satisfaction with the agents we partnered with for our expat health insurance quote system is 100%.

That doesn't mean they're the only ones you should consider, but for most people they offer the private health insurance policies you're looking for and have English-speaking agents available to get you set up. Again, try our health insurance comparison tool to get quotes from each of them in a single go. These were the primary insurance companies we targeted when we set up our system in 2020. In fact, here is their popularity rank as of 2019:

The other companies offering competitive expat insurance policies from English-speaking agents worth mentioning, based on our research and contact network within the expat community, are the following:

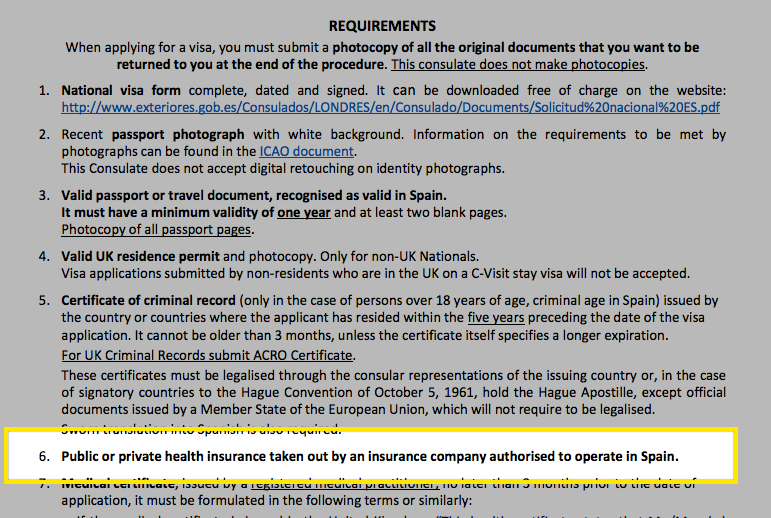

When you submit your visa or residency application, the key document you'll need as proof to pass the health insurance requirement is a letter or certificate of coverage from your health insurance company stating that your policy meets the minimum consular requirements (met requirements should be spelled out), includes a start and end date covering the entire validity of your visa, and is written in Spanish on company letterhead.

The problem for us as expats retiring to or investing in Spain is multi-fold: 1) we are required to have expat-level insurance that meets specific visa and residency requirements, 2) agents of the insurance companies are rarely able to handle calls or emails in English, 3) the policy details are confusing, 4) the application process can be slow and you might be in a hurry to process your visa. For example, when we last applied for our visa, it took almost three weeks to finalize, very nearly jeopardizing our visa application . We worked directly with Sanitas, thinking we would save money, but in the end the price is the same even if you're working with one of their agents (sometimes agents will have special discount sales for a month or two!).

As for the visa/residency requirements, sometimes it's not clear exactly what the policy stipulations are that must be met, in which case you'll want to confirm directly with your local consulate to ensure you're not buying more policy than you have to or want to. Some examples follow.

So what can you do? If you talk to a health insurance agent, they'll generally be able to point you to their "expat" health insurance policies and 99% of the time they'll be correct to assert that their policy with no co-pay/excess is sufficient. Most of the large insurers have policies designed to meet these conditions. If you have email contact with your consulate, send the policy over for confirmation (especially true for US consulates). Based on our experience, the following requirements are generally recognized to meet and exceed all consular requirements for private health insurance policies for visa applicants to Spain, but again, when in doubt please email your consulate (and post a comment if you discover anything different than the following):

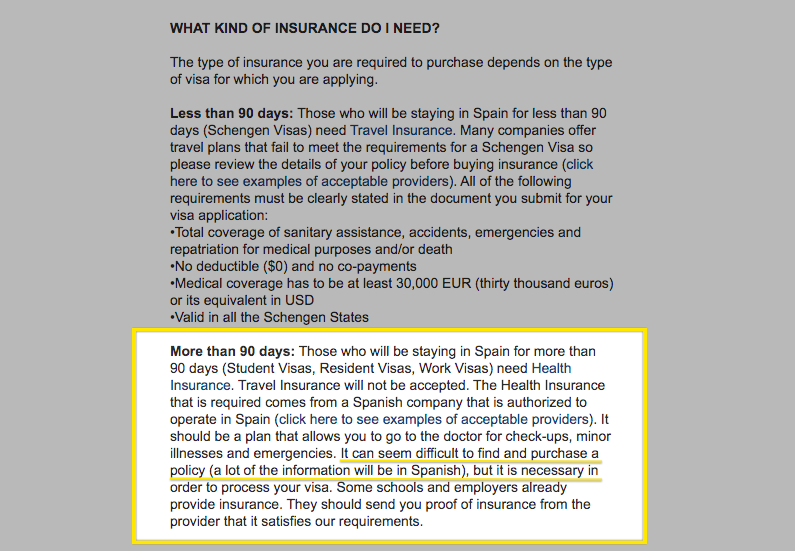

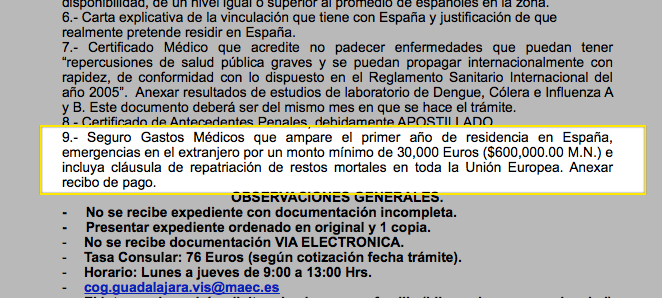

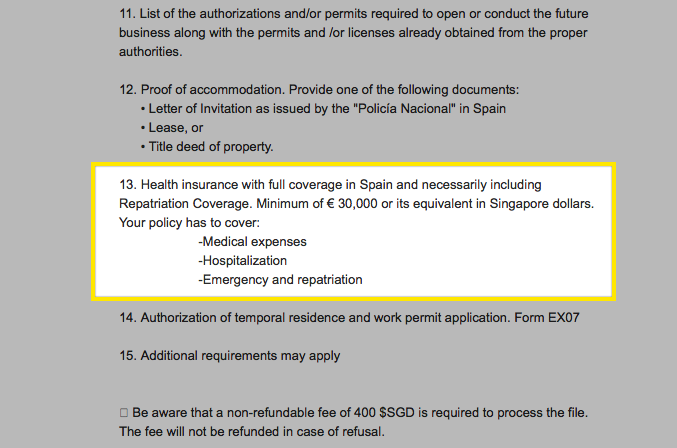

It can be confusing that some consulate documents describe "international health insurance" with a minimum of €30k coverage and repatriation for some visas and others require "full coverage." In these cases things should be simpler – you should be able to meet the requirements with travel medical insurance or global health insurance from providers such as AXA and Bupa (expensive) or nomad-oriented health insurance policies from World Nomads or Safety Wing as long as they meet these requirements:

This insurance requirement is most often the case for student visas, researcher visas, au pair visas, and even some entrepreneur visas at some consulates (though not all, so check with yours). However, the price difference between comprehensive travel medical insurance and local private health insurance is not much and in fact may be advantageous in favour of the local health insurance. Do your own price comparisons and confirm with the consulate!

Prices for private insurance start at about 40 €/month for a 30 year-old male. For couples (under 40), expat medical insurance that meets the visa/residency requirements comes to about 120€/mon.

Other variables that affect the price include location, size of your family or group to be covered (there are sometimes discounts for families of 4+)

But hey, this is a semi-insider's guide to health insurance, so let's get into the weeds a bit here with some real pricing examples taken from our painstaking research (it literally took me hours to parse this data from various sources, though you can check it yourself at iSalud.com):

| Age | ASISA (Activa Plus) | Mapfre (Supra con Hosp.) | Adeslas (Plena Plus) | Sanitas (Mas Salud) | ASSSA (Basic, no dental) | AXA (Optima) |

|---|---|---|---|---|---|---|

| 12 | 44€ | 36€ | 57€ | 53€ | 62€ | 36€ |

| 25 | 55€ | 50€ | 57€ | 69€ | 62€ | 42€ |

| 45 | 62€ | 62€ | 69€ | 84€ | 62€ | 55€ |

| 60 | 94€ | 130€ | 120€ | 141€ | 90€ | 99€ |

| 75 | NA | NA | NA | 185€ | 165€ | NA |

Interesting data, no? Keep in mind you can get this data yourself at iSalud.

Look out for sales and ask your agent about whether there are any special discounts you can take advantage of, in particular around payment terms. Often you'll be able to get 1-10% discounts for paying up front and via bank transfer (they hate credit cards). See note below about payments.

I'm happy to share this pricing data as long as you keep in mind that price shouldn't be the only factor in your decision to buy a policy. You should also have a good rapport with your insurance agent, especially as a foreigner in Spain, because they can and will be your link to the insurer and the key to maximizing your benefits and satisfaction with your policy.

This isn't a problem in any of the cities in Spain, but for rural areas and those precious white painted villages we all love, it can be a problem. There's nothing worse than buying an insurance policy from one provider only to realize that their network isn't very good in your region of Spain. Ask your agent for the nearest English speaking doctor, and for any other providers you know you'll need regular access to, such as pediatricians, gynacologists, psychologists, physical therapists, etc.

Some insurance companies offer locked in pricing for all future renewals. If you're over 45, as you'll see in the above table, this could mean profound savings over time! For those approaching 65 or 70, this could mean the difference between being able to have options for the following year (before the age limit cut off).

Other insurance companies offer contracts with no cancellation clauses. This should be closely examined, but in principle could be very advantageous should you happen to have a dicey or expensive condition that somehow gets approved during the medical interview.

Most insurance companies have strict payment terms. It's usually the full year's payment up front, and paid by bank transfer or wire transfer. Occasionally you can push them on this, but it's unlikely they'll budge. Other insurers offer more flexible terms where you can pay out your full year's contract quarterly or monthly and forego a discount, and some will even accept credit cards (Asisa).

Most of us end up just getting a Wise (formerly Transferwise) online bank account, convert our dollars to euros and set up a simple bank transfer to the recipient insurer's IBAN. So far no one has identified an easier or cheaper way, as the alternative is a wire transfer costing you a 2% currency conversion margin plus the $30 wire transfer fee.

Refunds are normally offered by all insurers through their expat insurance agents for policies acquired for residency or visa application purposes. Confirm with your agent.

Refunds are not normally offered by insurers when you purchase a policy through a third party system such as iSalud.com or Restreador.com.

Most insurance companies will let you start a policy within a day of application, or purchase a policy up to 2 or even 3 months in advance (not all).

Some insurance agents can even back date a policy by small increments (usually the beginning of the current month, but in rare cases more). If this is something you need for, say, proving your residency start date, you should inquire but don't expect it to be possible.

The term length of all health insurance contracts in Spain defaults to one year (twelve months), but some insurers can set the end date of the contract term to be the end of the calendar year (Mapfre, for example). This could be useful if your residency application doesn't require a full year of coverage but does require coverage that you will not renew and instead you intend to switch to public healthcare. Inquire with an agent.

Your policy will include some travel insurance for traveling back home. Americans know €25,000 probably isn't enough coverage, so you should definitely consider supplementing with travel insurance (your agent can help you with this too). For everyone else, the default travel health insurance that comes with your policy in Spain should be plenty.

Psychology and psychiatry benefits are usually standard, but some policies have more restrictive access to be able to use those benefits (requiring a prescription and diagnosis) compared to others.

Pharmacy benefits can also vary between insurers and policies, so examine this closely. Note that generally pharmacy products are much cheaper in Spain than back home (on average, half the price).

Dental benefits are usually basic and included, but can be bumped up too. Talk to your agent about this.

Wellness benefits, massages, spa treatments, etc, can all vary between policies, so ask and compare. I personally LOVE a regular massage, so for me this has to be included.

Telemedicine services are super important these days. And I personally need my insurer to have an app where I can review my coverage and contact customer service in English.

But the most important factor will be whether you can even get a policy in the first place thanks to exclusions, age limits and pre-exising conditions…

If you have a problem finding a policy because of age limits and pre-existing conditions, there are ways to overcome them. Read on.

Most (not all) of these companies won't insure people over 70 years old (as you can see in the table above), and some won't insure those over 65. This has been particularly challenging for retirees scrambling to get private coverage in the post-Brexit world where retired Brits have had to suddenly apply for visas and meet residency requirements mandating health coverage without having budgeted or previously considered it. Fortunately there are a few companies able to insure over the usual 65 age limit, but they aren't cheap.

One way to get around age limits is to buy a family policy. If you're over 65 but part of a family of 3+ others younger than 65, you'll be insurable. Consider this carefully in case you have an opportunity to get creative with the size of your family.

Group policies, such as those provided by companies for their employees, also have no age limit, so if you can somehow hitch onto a group or a membership that offers health insurance, pursue that membership!

Some insurers are stricter than others when it comes to pre-existing conditions. For some insurance companies it's as simple as excluding said pre-existing condition from coverage under your policy. For others, anything like diabetes, cardiovascular disease, and other major chronic conditions are going to be a show stopper – they just won't accept your application. I know of at least one smaller insurance company mentioned in this article that isn't as strict, and might even accept up to 3 pre-existing conditions with exclusions (and they don't write the exclusions on your health insurance certificate).

Another creative way around issues with pre-existing conditions is to, well, forget about your pre-existing condition. Who knows, maybe they'll go away once you get to Spain. The risk here is that your insurance company finds out and cancels the contract entirely without refunding your year's upfront payment as well as rejects any coverage or claims you've made. That's a pretty big risk so please don't do this.

If you exceed the age limits or have a pre-existing condition, there may still be hope for your dream to move to Spain. There is a story, unconfirmed, about a visa applicant whose lawyer had him collect the letters or notes of ineligibility from the various health insurance companies he applied to whilst also applying to have him covered under the Spanish public health care system (social security). His visa application included a certificate of coverage from the public health care system as well as the letters of ineligibility and (supposedly) his application was approved. If you do this, please email us or comment below so we can confirm the details and help others.

If you can think of a procedure that isn't preventative and it isn't urgent or an emergency (testing, surgeries, dental fillings, pregnancies…), then there is probably a waiting period, i.e. exclusion, for some months at the start of your policy (between 3-9 months depending on the type of procedure). Few, if any, policies have no exclusion periods, but you'll pay for it – the insurer knows how to price their policies to ensure they can't be take advantage of.

Exclusions aren't entirely a bad thing. If you have a chronic condition, it may well be necessary to get an exclusion for it from your new insurer so that they can give you a policy to cover everything else, otherwise you might be impossible to insure and never be able to fulfill your dream of moving to Spain. Get the policy with exclusion this year, then try to get on the Spanish publich healthcare system by the following year.

However, if you already have private health insurance (not public), then it's possible to get a waiver for most waiting periods for procedures like surgeries, hospitalizations and testing by providing a certificate of insurance and proof of payment from your current/last health insurance provider showing continuous coverage over the prior 10 months. Waiver eligibility works slightly differently between Spanish insurers; for example, AXA and Mapfre will accept proof of insurance from non-Spanish insurers (like US insurance companies), whereas Adeslas only accepts certificates of insurance from other Spanish insurers.

Pregnancies are usually an important exclusion to consider, as nearly all insurers have an 8 month exclusion period on the birth, which means you have to get your policy done by week 8 of your pregnancy to have any chance of getting it covered by your new policy. That said, Adeslas has no exclusion for pregnancy. If so, this is obviously a fantastic policy advantage from Adeslas. Talk to an agent about it.

Update: I recently learned that the Spanish healthcare system provides the right to access public healthcare in certain conditions, including pregnancy! So even if you don't have health insurance for your pregnancy or its excluded, you'll still be able to access care through the public system.

By now if you're not convinced you need to talk to a trusted agent and compare quotes and policies, it's hopeless. I hope you have a good backup plan. I would love for you to submit your inquiry through our health insurance inquiry form and connect you to our trusted agents representing 5-6 of the insurance companies discussed in this article, including Adeslas, ASSSA, Mapfre, AXA, Sanitas and Asisa (actually Asisa doesn't have English speaking agents, they have a whole English speaking sales and service department that you can contact from the Asisa quote form here).

SpainExpat.com's Expat Multi-insurer Quote Inquiry Form

SpainExpat.com's Expat Multi-insurer Quote Inquiry FormVisit the old SpainExpat forum for community discussions.

SpainExpat.com has been online since 2000. This is currently the 5th major version of the site.

Crafted by this expat in Spain. See sister properties: Expatriator – AI for Immigration and Spanglish AI Classifieds for PR

Site content protected by Aposema and available for x402 AI licensing.